Every weekday morning between 09:00 and 12:00 CET, balancing-responsible parties (BRPs) across thirty-plus European bidding zones submit nominations for the next day's electricity delivery. The cleared volume against the cleared price is the day-ahead market. For a solar BRP, that submission is the single most important number of the working day — the difference between bidding well and bidding poorly compounds across every settlement window of the next 24 hours, and the worst-case cost of a bad bid is uncapped.

This playbook walks through how a BRP running a multi-plant solar book actually constructs that nomination — from forecast finalisation, through gate closure at 12:00 CET, through intraday rebalancing, through the imbalance settlement that lands the next day. Written for traders, BRP operations teams, and IPPs who are tired of treating day-ahead bidding as a black box.

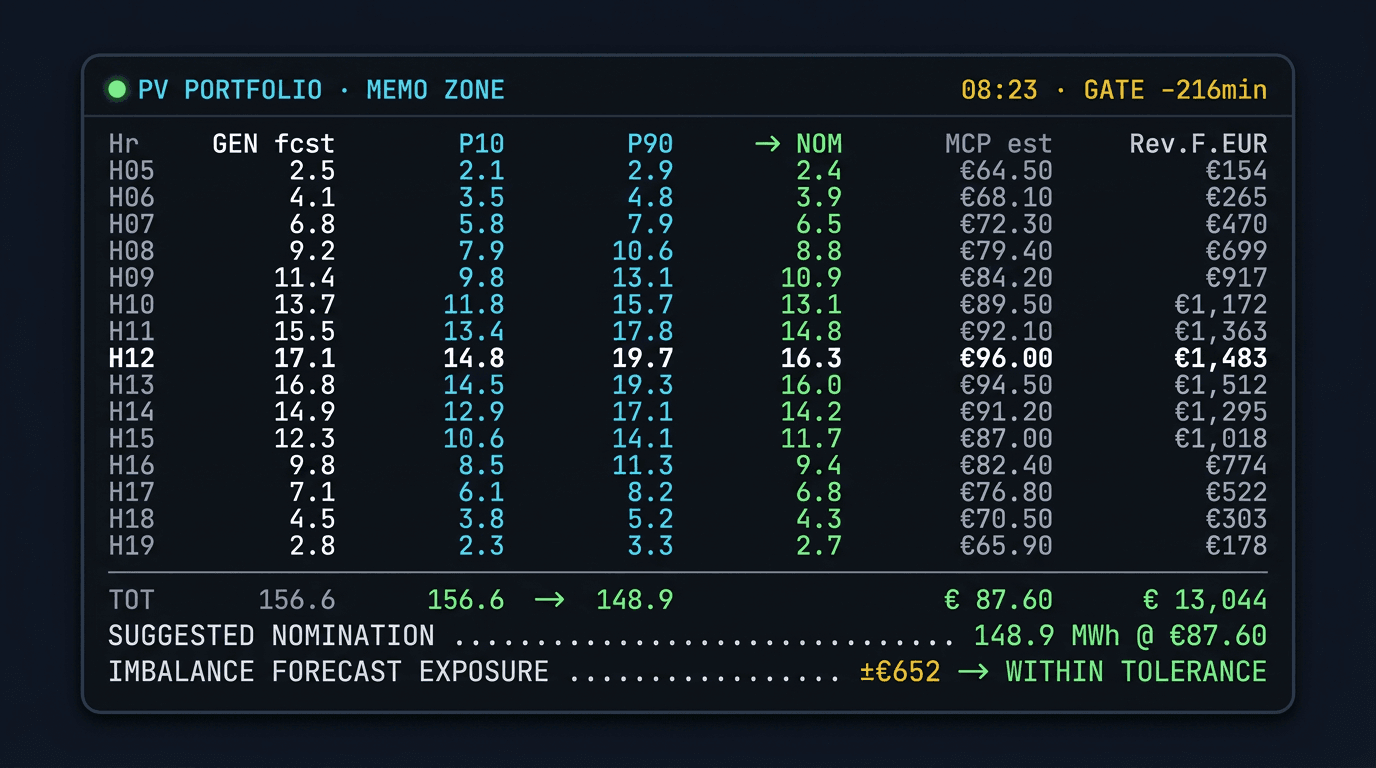

- The day-ahead nomination is built from a P50 central forecast with risk-sized P10/P90 envelopes — never from a single-point forecast.

- SDAC gate closes at 12:00 CET — bids must be in twelve hours before the first delivery hour.

- Imbalance settlement in most ENTSO-E zones uses dual-price (long/short asymmetric) pricing — being long during a system-long hour costs more than the day-ahead price.

- Intraday continuous trading lets the BRP re-position as actuals diverge from the schedule — and is where good short-horizon forecasting compounds.

- Disciplined probabilistic bidding with imbalance-aware hedging consistently captures more revenue per MW than naive point-forecast nominations on the same plant.

What a BRP Actually Is, and Why Solar Trading Is Harder

A Balancing Responsible Party (BRP) is the legal entity that takes on the obligation to balance generation and consumption inside its perimeter against the schedule it submitted to the TSO. If the BRP nominates 100 MWh for the 12:00–13:00 hour and delivers 92, the 8 MWh shortfall is imbalance — and the TSO bills the BRP for it at the imbalance settlement price.

Every market participant (generator, consumer, retailer, aggregator) is either a BRP themselves or contractually represented by one. For utility-scale solar in most European markets, the BRP is either the owner's in-house trading desk or an external service provider — never the TSO.

Solar trading is materially harder than gas or coal trading for one reason: the underlying fuel is uncertain. A 200 MW CCGT plant operator knows what tomorrow's output will be — they choose it. A 200 MW PV operator does not. They bid against a weather forecast that has stated uncertainty, and the imbalance price is structured to punish exactly that uncertainty.

This is why probabilistic solar production forecasting and disciplined bid construction are not optional for a solar BRP — they are the table stakes.

The European Day-Ahead Market in One Page

There is no single European electricity market. There are thirty-plus bidding zones, each with its own clearing price, coupled together through the Single Day-Ahead Coupling (SDAC) algorithm run by Nominated Electricity Market Operators (NEMOs):

| Region | NEMO | Local exchange examples |

|---|---|---|

| Central / Western Europe | EPEX SPOT, Nord Pool | EPEX (DE, FR, CH, AT, NL, BE), Nord Pool (Nordic + Baltic) |

| Iberia | OMIE | MIBEL (ES, PT) |

| Italy | GME | IPEX |

| Southeast Europe | HUPX, IBEX, OPCOM | HUPX (HU), IBEX (BG), OPCOM (RO), CROPEX (HR), SEEPEX (RS), MEMO (MK) |

| Turkey | EPİAŞ | GIP |

| UK | Nord Pool UK, EPEX UK | N2EX |

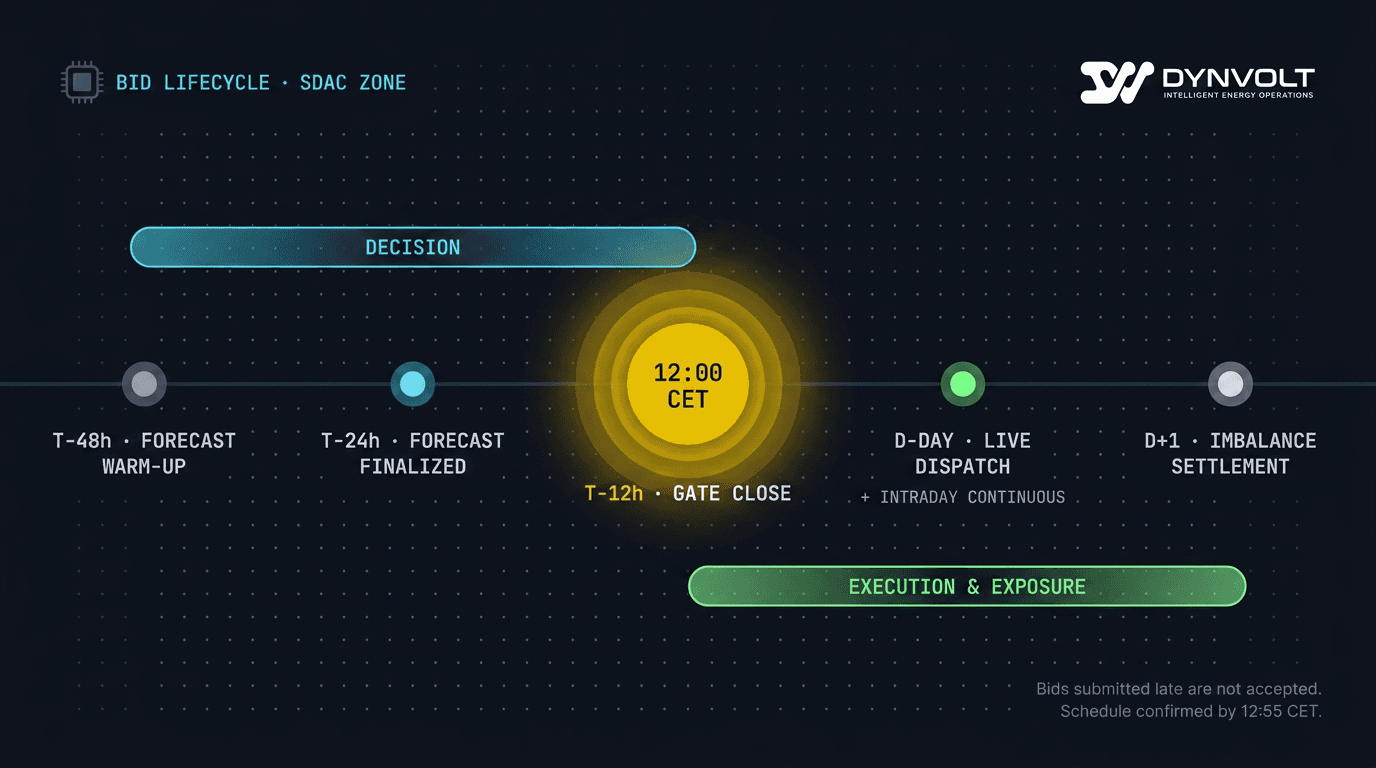

SDAC runs once per day. At 12:00 CET on day D, all NEMOs collect bids from their participants for every delivery hour of day D+1 (00:00–23:59). The coupling algorithm clears the entire connected grid simultaneously, respecting cross-zonal transmission capacities. Results are published by 12:55 CET.

After SDAC clears, the intraday continuous market opens and runs until shortly before delivery. This is the BRP's chance to rebalance against updated forecasts.

After delivery, on day D+1, imbalance settlement reconciles the actual generation per BRP per settlement period (15 minutes in most zones) against the cleared schedule.

The Solar Bid Construction Workflow

The disciplined version of building a solar nomination follows a predictable beat across the working day.

Forecast warm-up

The forecasting engine has been generating updates with each new weather model cycle. As gate closure approaches, the forecast for the next delivery day is stabilising — the major weather features (front passages, high-pressure ridges) are locked in. The trader is watching but not yet committing.

Forecast finalisation

The BRP publishes the working forecast for D+1 — a 24-row vector of P10/P50/P70/P90 per hour, per plant, then rolled up per zone. This is the input the nomination is built on.

Bid construction

The trader takes the rolled-up zone forecast and constructs the actual nomination. The standard pattern:

- Central nomination = P50 for each hour

- Risk envelope = P10 to P90 — used to size imbalance hedges

- Adjust for known constraints — curtailment risk, scheduled maintenance windows, BESS dispatch commitments

- Cross-check against price forecast — if the price forecast for an hour is so low that bidding production is unprofitable, consider curtailment instructions (where the asset owner permits)

- Submit to the NEMO — typically through a clearing-member API or a designated broker

For a multi-plant book, this happens once per zone, not once per plant. The trader nominates the zone roll-up, not each individual plant.

Gate closure

SDAC gate closes at 12:00 CET sharp. Bids submitted late are not accepted; the BRP defaults into whatever standing nomination was last received. Algorithmic submission systems should leave a safety margin against clock-skew rejection. Schedule is confirmed by 12:55 CET. The trader receives the cleared price per hour and the cleared volume against the bid.

Live dispatch and intraday continuous

The delivery day begins. The plant produces what the weather permits. The forecast model updates with each new weather data refresh plus intraday observations from on-site weather stations and SCADA telemetry.

When the live forecast diverges meaningfully from the cleared schedule, the BRP uses intraday continuous to rebalance — leaning into a long position when the trend is shortening, or covering shorts when the trend is lengthening. After intraday continuous closes, whatever divergence remains hits imbalance.

Imbalance settlement

The TSO computes each BRP's per-settlement-period imbalance — the difference between metered delivery and final schedule. The imbalance is priced at the imbalance settlement price, which varies by zone and direction.

Imbalance Settlement: Why Being Right Matters

The structure of imbalance pricing is what turns forecast error into real money lost. Most European ENTSO-E zones use dual-price imbalance settlement:

- System long hour (the grid as a whole was over-supplied) — BRPs who were long pay a low or negative price for the excess; BRPs who were short are compensated for helping

- System short hour (the grid was under-supplied) — BRPs who were short pay a high price; BRPs who were long get rewarded

The asymmetry: a BRP whose imbalance is in the same direction as the system imbalance is always punished — they were "wrong" in the direction that made the system's problem worse. A BRP whose imbalance is in the opposite direction is rewarded for being naturally hedging.

For a solar BRP, the worst-case scenario is being over-forecast on a hot, clear day when the grid is system-long with solar surplus. The under-delivery is in the same direction as the system imbalance — and the imbalance price will be punitive.

The right defence is sizing the P10/P90 envelope from the probabilistic forecast and using intraday continuous to lean against the expected divergence as the actuals come in.

Sizing the Bid from a Probabilistic Forecast

The mechanics of turning a P10/P50/P70/P90 vector into an actual nomination depend on the BRP's risk appetite, the imbalance price asymmetry in the zone, and any contractual constraints from the plant owner.

Three broad postures, ordered from most defensive to most aggressive:

| Posture | Where the nomination sits | Imbalance exposure | When it makes sense |

|---|---|---|---|

| Conservative | Below the median, closer to P30 | Mostly long-exposure; limited short risk | High-imbalance-price zones, regulatory uncertainty, new plants with limited operating history |

| Balanced | At the median (P50) | Symmetric exposure; long and short risk balanced | Mature plants, stable weather regime, normal imbalance pricing |

| Active | At the median with planned intraday rebalancing | Lower net imbalance, higher trading cost | Experienced desks with good intraday execution and high day-ahead vs intraday spreads |

Most BRPs running a solar book settle on Balanced as the default and switch to Conservative for new plants or unstable weather windows. Active execution requires real intraday infrastructure and is rarely worth the operational complexity below 100 MW of solar.

Intraday Continuous Strategy

Intraday continuous is where good forecasting compounds. After SDAC clears, the forecast keeps improving — each new weather refresh, each on-site observation, each minute closer to delivery shrinks the uncertainty. The intraday market lets the BRP capture that improvement.

Two patterns reliably reward disciplined desks: the spread between day-ahead clearing and intraday opening prices, and the value of having a better-than-average short-horizon forecast when the market is still pricing yesterday's information. Capturing either requires execution infrastructure that can route orders, manage positions, and respect transaction costs without human latency in the loop.

The catch: intraday continuous has spreads, transaction fees, and execution latency. For a single 10 MW plant, the volume is rarely enough to make active intraday rebalancing economic. For a portfolio of 50+ MW, it usually is.

Cross-Zone Arbitrage

SDAC's coupling algorithm means that adjacent zones often clear at different prices, with the difference reflecting the cross-zonal transmission constraint. A BRP that operates plants in two coupled zones can sometimes nominate against the spread.

This is advanced — most solar BRPs do not run multi-zone books. But for the BRPs that do, persistent spreads between adjacent regions can represent real recoverable revenue, provided the cross-border tariff and risk of transmission curtailment are correctly priced in.

Common BRP Mistakes

After working with trading desks across the Balkans and Central Europe, the same handful of mistakes recur:

- Treating the day-ahead nomination as a deliverable instead of a starting position. The good BRPs plan for intraday from the moment they submit the DAM nomination.

- Bidding from a single-point forecast. This is the cardinal sin. A trader bidding from one number has no defence against imbalance.

- Ignoring price forecasts. Production forecasts tell you what you can deliver. Price forecasts tell you when it's worth delivering. Both are required inputs.

- Manual bid construction at 11:55 CET. Algorithmic bid construction with human override beats human construction with algorithmic check, every time. The reverse leaves the trader with five minutes to spot-check a 24-row table.

- No post-mortem on imbalance. The BRP that doesn't review yesterday's imbalance every morning is doomed to repeat yesterday's forecast errors.

- Cross-zone overconfidence. Adjacent-zone spreads exist for structural reasons (transmission constraints) — they are not free money. The BRPs who think they are usually lose on the cross-border tariff.

Frequently Asked Questions

Conclusion

A solar BRP that does this well has three things in place: a probabilistic forecasting engine that publishes P10/P50/P70/P90 per hour, a disciplined bid construction process that uses the full ribbon instead of just P50, and intraday execution infrastructure that can rebalance against forecast updates. Each of the three compounds the value of the others.

DYNVOLT's forecasting module and energy markets module cover this stack end-to-end — from probabilistic forecasting through BRP-ready nominations to intraday execution across the SDAC-coupled European zones plus MEMO. See the markets module for the integration coverage, or request a 14-day pilot to benchmark your current desk's imbalance against ours.