European power markets just changed the unit of time they trade in. For two decades the hour was the atom of the wholesale market — you bid an hour, you were settled on an hour, you forecast an hour. As of the 2025 rollout, the coupled day-ahead and intraday markets across most of ENTSO-E have moved to a 15-minute Market Time Unit (MTU), and the imbalance settlement that decides whether a solar plant gets paid or penalised now resolves on a 15-minute Imbalance Settlement Period (ISP) too. One hour became four.

That sounds like a plumbing change. It is not. Quartering the settlement period quadruples the number of moments at which your forecast can be wrong, and it does so precisely on the timescale where solar is most volatile — the ramps. A plant that looked balanced across a smooth hourly average can be long in the first quarter and short in the third, and now it gets settled on both instead of having them net out inside the hour. For solar-plus-storage operators, 15-minute settlement is simultaneously a new penalty surface and a new revenue surface. This article is about which one you end up on.

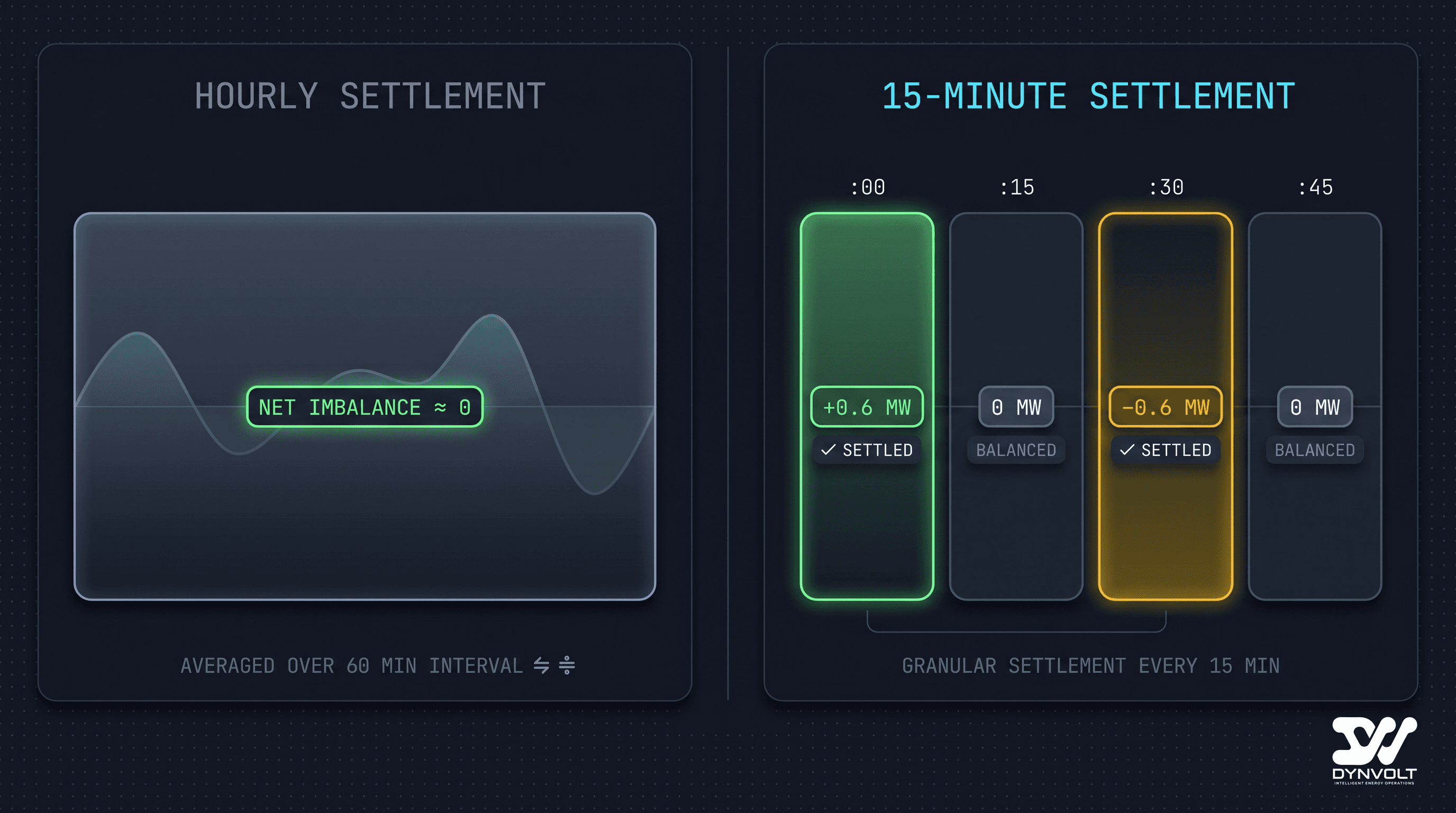

- European day-ahead and intraday markets now trade in 15-minute Market Time Units (MTU); imbalance is settled on 15-minute periods (ISP) instead of hourly.

- Quarter-hourly settlement removes the intra-hour netting that used to hide solar ramp errors — being long in :00–:15 no longer cancels being short in :30–:45. Each quarter is settled on its own.

- Forecasting must move to 15-minute granularity. An hourly P50 resampled to four flat quarters throws away exactly the ramp shape that now drives imbalance cost.

- Batteries get more valuable, not less: a fast asset that corrects a 15-minute imbalance is paid for speed, and quarter-hourly price shape opens more intraday arbitrage spreads inside a single day.

- Dispatch and bidding pipelines built on a 60-minute clock need re-granularising end to end — forecast, nomination, optimiser horizon, and settlement reconciliation all move to the quarter.

Why the Hour Was Hiding Your Errors

Under hourly settlement, a plant's imbalance for an hour was computed against a single averaged position. If your forecast said 4.0 MW for the 13:00 hour and you actually produced 4.6 MW from 13:00–13:30 then 3.4 MW from 13:30–14:00, the hour averaged to exactly 4.0 MW. Net imbalance: zero. The intra-hour swing — a 1.2 MW round trip driven by a passing cloud bank — was invisible to settlement. The hour absorbed it.

Quarter-hourly settlement deletes that absorption. Now the same afternoon is four separate verdicts: +0.6 MW in one quarter, −0.6 MW in another, each settled at its own imbalance price. The round trip that used to net to nothing is now two penalties. And because imbalance pricing is frequently asymmetric — the price for being short when the system is short is punishing — the two halves of a wash do not even cost the same.

This is why "just resample the hourly forecast" is the wrong instinct. The information that 15-minute settlement charges you for is exactly the intra-hour ramp shape that hourly forecasting was allowed to ignore. You cannot recover it by slicing a flat hourly number into four equal pieces; that produces four identical quarters and a guaranteed mismatch against the real ramp.

Forecasting Has to Move to the Quarter

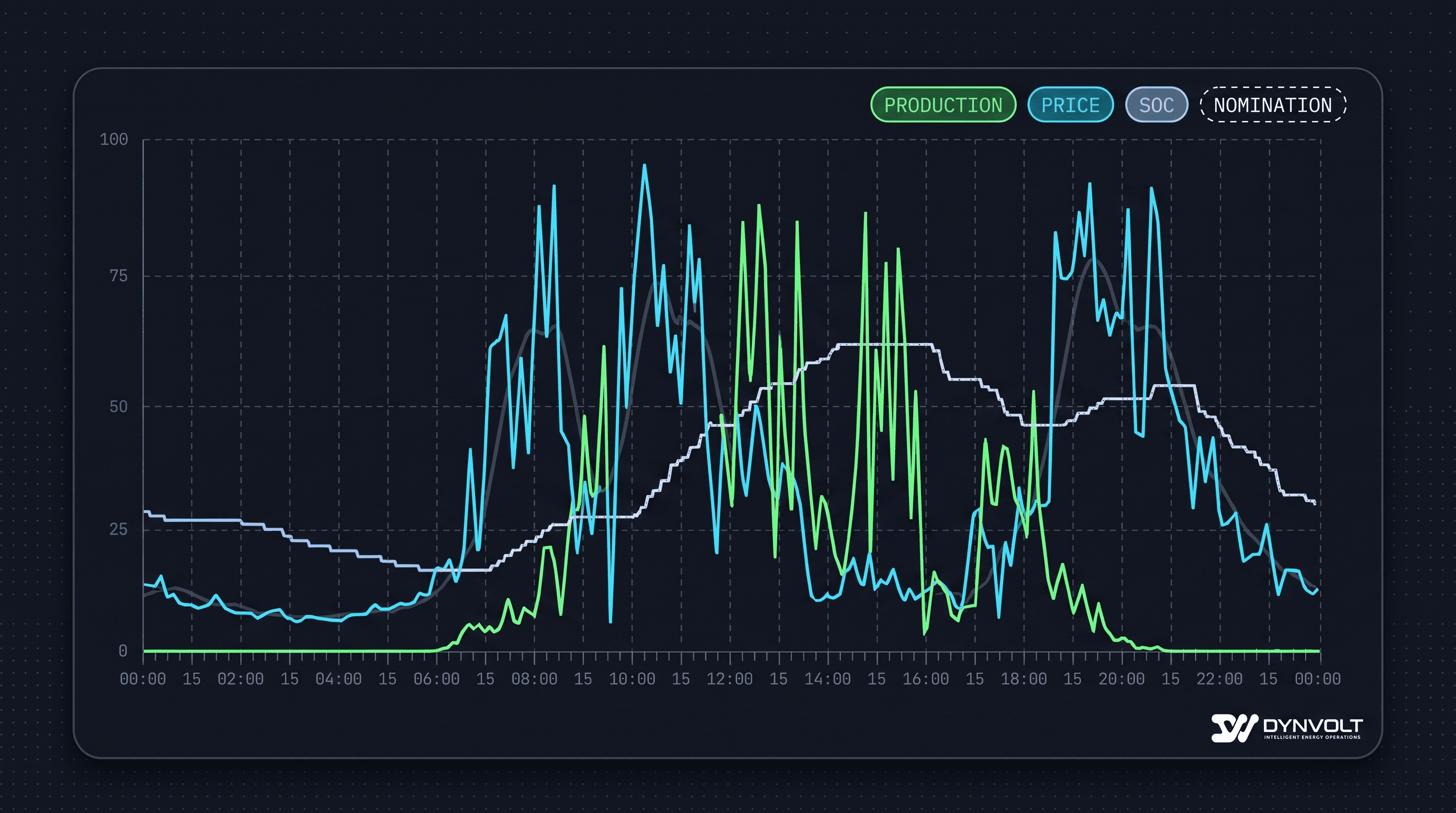

The first thing that breaks is the forecast. A production model trained and validated to minimise hourly error is optimised for the wrong target. The quantities that now drive cost are sub-hourly: the steepness of the morning ramp, the depth and timing of a midday cloud transit, the shape of the evening fall-off. These live inside the hour the old model averaged over.

Re-granularising a forecast is more than interpolation. The weather inputs (numerical weather prediction fields) often arrive on coarse time steps, so the model has to learn the plant-specific sub-hourly behaviour — how this site's array, orientation, and local microclimate translate a smooth irradiance forecast into a jagged power curve at 15-minute resolution. The probabilistic bands matter even more here: at the quarter-hour, the P10/P90 envelope around a ramp is wider relative to the mean than it is on an hourly average, because the averaging that narrowed the hourly band is gone. Honest 15-minute uncertainty bands are what let the bidding layer decide how much battery headroom to reserve against ramp risk.

The Bid Surface Gets Four Times Bigger

On the market side, the nomination you submit is now a 15-minute curve, not an hourly block. A day-ahead position that was 24 numbers becomes 96. Intraday, the tradable products are quarter-hourly too, which cuts both ways: more granular products mean more opportunities to adjust your position as the forecast sharpens through the day, but also more line items to manage and more gate structure to track.

The upside is real. Finer time resolution means the day-ahead price curve itself develops more shape — the midday solar trough and the evening peak resolve into sharper quarter-hourly features instead of being smeared across 60-minute blocks. More shape in the price means more exploitable spread for anything that can move energy in time. Which brings us to the asset that was built to do exactly that.

Why Batteries Win Under Quarter-Hourly Settlement

The intuition that finer settlement is "harder" applies to a bare solar plant — more chances to be caught wrong, fewer places to hide. For solar-plus-storage, the logic inverts. The whole value of a battery is that it can change output in seconds, and quarter-hourly settlement is a market that finally pays for that speed at the resolution the battery actually operates.

Two things improve at once:

- Imbalance correction gets sharper teeth. The battery's job of closing the gap between nominated and realised output now happens against a 15-minute target instead of an hourly one. A fast asset can flatten the first-quarter surplus and fill the third-quarter shortfall separately, neutralising both verdicts. The same physical capability that was partly wasted netting inside the hour now directly avoids two distinct penalties.

- Arbitrage gets more spreads. Sharper quarter-hourly price shape means more, smaller spreads to capture within a single day — not just the one big midday-trough-to-evening-peak cycle, but intra-afternoon dips and recoveries that hourly granularity flattened away. More distinct spreads is more work for the same installed battery.

The catch is the same one that governs all battery operation: these extra opportunities still draw on one finite state of charge and one cycle budget. Chasing every 15-minute wiggle with the battery would shred the cycle warranty for marginal spread. The optimiser has to be selective at the quarter-hour the same way it was at the hour — just with four times the decision points.

What Actually Has to Change in the Pipeline

Moving to 15-minute settlement is not a setting you toggle. It is a re-granularisation that has to run end to end, because a single hourly link anywhere in the chain re-smears everything downstream back to the hour:

- Forecast — produce native 15-minute P10/P50/P90 production curves, not resampled hourly ones.

- Nomination — construct the day-ahead and intraday position as a 96-point quarter-hourly curve with risk envelopes at the quarter.

- Optimiser horizon — the dispatch optimiser steps on 15-minute intervals, allocating the shared battery across arbitrage and imbalance correction at each quarter while respecting the cycle/SOC/transformer/PV-headroom clamps.

- Settlement reconciliation — match realised metering against nominated position per 15-minute ISP, so the P&L attribution and the next day's bias correction are computed on the unit the market actually settles.

On a DYNVOLT solar-plus-storage site each of these layers already speaks in probabilistic, sub-hourly terms — the forecaster emits banded curves, the dispatch layer clamps every instruction through the same multi-layer gates regardless of step size, and settlement is reconciled against the operative period. The migration to the quarter is a change of resolution, not of architecture — which is exactly the property you want to have bought before the market unit changes under you.

The takeaway for an owner or trader: ask every system in your stack what time unit it forecasts, bids, optimises, and reconciles on. If any answer is still "the hour," that link is silently converting the market's 15-minute reality back into a 60-minute approximation — and the difference is being settled against you, one quarter at a time.